Getting on top of your finances can feel daunting, as random expenses pop up out of nowhere every time you start to save. Even thinking about your debt is so stressful you tend to shove it to the back of your mind.

Take a deep breath. There is a path forward.

At RaiseUp Families, we care deeply about families experiencing financial hardship. Our programs are designed to help parents provide a stable home and education for their children.

In today’s blog, we’ll explore financial goal-setting, breaking it down into doable steps. We’ll also explore resources where you can find more in-depth information and access financial counseling.

Let’s get started!

When you’re living paycheck to paycheck, you’re so worried about having enough money for groceries this week that it’s easy to have a short-term mindset about money. If you have extra cash, it’s easy to spend it on a slightly extravagant meal or a cute new pair of jeans because you can afford it.

The problem?

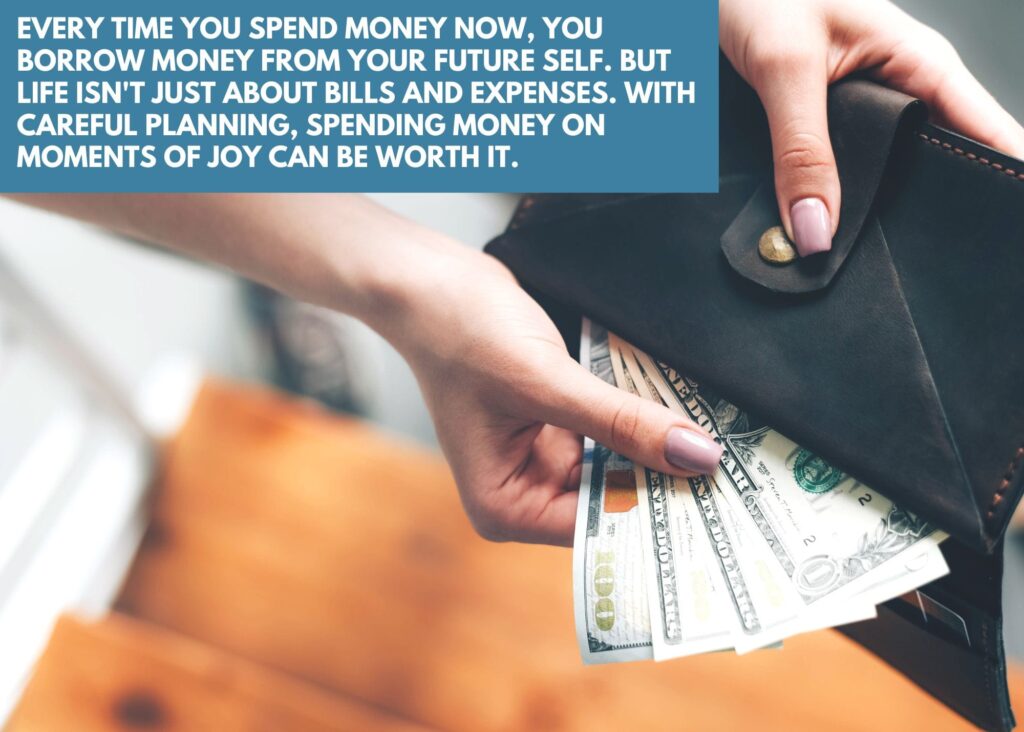

Every time you spend money now, you borrow money from your future self. Just because today-you can afford it doesn’t mean future-you can afford it. What if you have to pay a parking ticket? What if your work hours get cut?

Of course, life isn’t just about bills and expenses. It’s worth it to spend money on moments of joy. But when you keep future-you in mind, that joy might look different. For example, you may realize you’d happily give up your daily treat if it meant being able to go on vacation with your family or buy your children something extra special for Christmas.

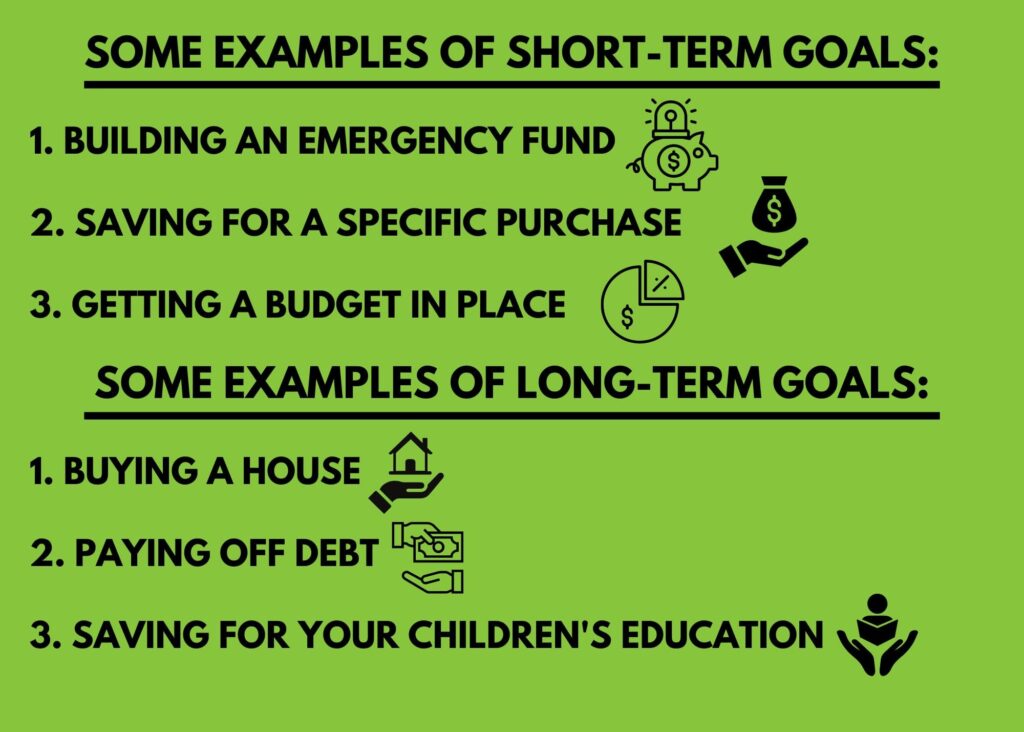

Saving for a vacation or the holidays is an example of a short-term financial goal. As you get into the habit of thinking long-term, it will become easier to set financial goals, including long-term goals like saving to start your own business or helping your children pay for college.

Let’s look at some more examples of short-term and long-term financial goals.

As we explore options of short-term and long-term financial goals you may want to pursue, don’t let the list overwhelm you. These aren’t things you have to figure out all at once. Instead, as you read the list, allow yourself to believe these goals are possible, and get excited!

Short-Term Goals:

Long-Term Goals:

Let’s imagine that you want to save money to buy a car. Your financial goal is to eat out less and put that money toward your car. But at the end of the year, you only have a couple hundred dollars saved—nowhere near enough to buy a reliable vehicle.

What happened?

We can analyze why this goal failed using the SMART goal framework. SMART is an acronym for Specific, Measurable, Achievable, Relevant, and Time-Bound.

Specific: Try to be more specific than “I want to buy a car.” What kind of car do you want? What does it need to accomplish?

Measurable: Your goal should be measurable, with a specific dollar amount. For example, “I want to save $10,000 this year to buy a reliable used car.” That way, you can create benchmarks and know if you’re hitting them.

To save $10,000 a year, you’d need to save $833.33 a month. That’s a specific, measurable amount you can work towards.

Achievable: Now it’s time to ask yourself – is it realistic, given your expenses and income, to save $833.33 a month by cutting back on eating out? Since the average household spends around $300 per month eating out, this is likely not an achievable goal for you. No wonder your earlier attempt failed so spectacularly!

Look at where you spend your money, and figure out where you can realistically cut back. Maybe you can manage to save $400 a month. In that case, adjust your goal to something more achievable: saving $7000 for a car in a year and a half.

Relevant: Now it’s time to pause for a moment, think about your financial needs, and make sure that getting a car is your top priority. For example, if you don’t have an emergency fund, you should focus on that first.

Time-Bound: Finally, make sure your goal has a specific time frame. In our example, that time frame is a year and a half, meaning you’ll aim to save $388.89 per month. Since your goal is time-bound in this way, you’ll have some sense of whether or not you’re on target every month.

Now that we understand the types of goals we might want to set and the SMART goals framework for setting them, let’s go through the goal-setting process step by step.

Step 1: Assess your finances

Start by examining your monthly spending, including how much you spend on groceries, eating out, clothing, rent, subscriptions, and other expenses. This will help you set achievable goals based on where you can realistically cut back on spending.

Step 2: Start small

You’re probably excited about your financially-stable future, and ready to start saving for all the things. But if you get carried away, you’ll set yourself up for failure and disappointment.

Start by setting 1-3 short-term goals and devising a plan. When in doubt, set smaller goals rather than bigger ones. Consistently saving $10 a week will motivate you and give you a sense of control, whereas failing to save $100 per week will make you want to quit.

Step 3: Come up with a plan based on the SMART framework

Using the SMART framework we reviewed earlier, refine your small goals until they are specific, measurable, achievable, relevant, and time-bound.

Step 4: Involve others in your plan

You’re much more likely to achieve your goals if you involve others in your plan. Team up with a friend, make goals together, and hold each other accountable.

Step 5: Assess and adjust your goals

After a few months of following your plan, it’s time to reassess. Are you realistically able to save as much as you’d hoped? If not, try setting your money-saving goals a little lower. If it’s going well, maybe see if you can save a little more.

You may also want to re-adjust your priorities. For example, if you realize that you’ll need a new furnace before winter, you may switch from saving for a car to saving to buy a new furnace.

Step 6: Transition from short-term to long-term goals

At first, your saving goals will probably center around short-term, immediate needs, like making sure you have an emergency fund, reliable transportation, and basic health needs covered. But as you start to find success with taking care of those immediate needs, it’s time to start thinking about future-you and taking care of those long-term needs.

To achieve long-term goals like paying off debt, building wealth through investments, and saving for your children’s education, follow the steps outlined above—assess your finances, start small, use the SMART framework, involve others in your plan, and periodically assess and adjust your goals.

Setting financial goals sounds simple on paper: assess your finances, figure out how much you can save, and budget accordingly.

But in reality, it’s complicated. Despite our best efforts, money tends to slip through our fingers. We may be overpaying for rent or insurance and have no idea, or be conned into spending money on useless investments.

Maybe you want to eat out less, but your friend group’s go-to activity is to try new restaurants. Perhaps you have a gambling or shopping addiction that rears up whenever you’re stressed.

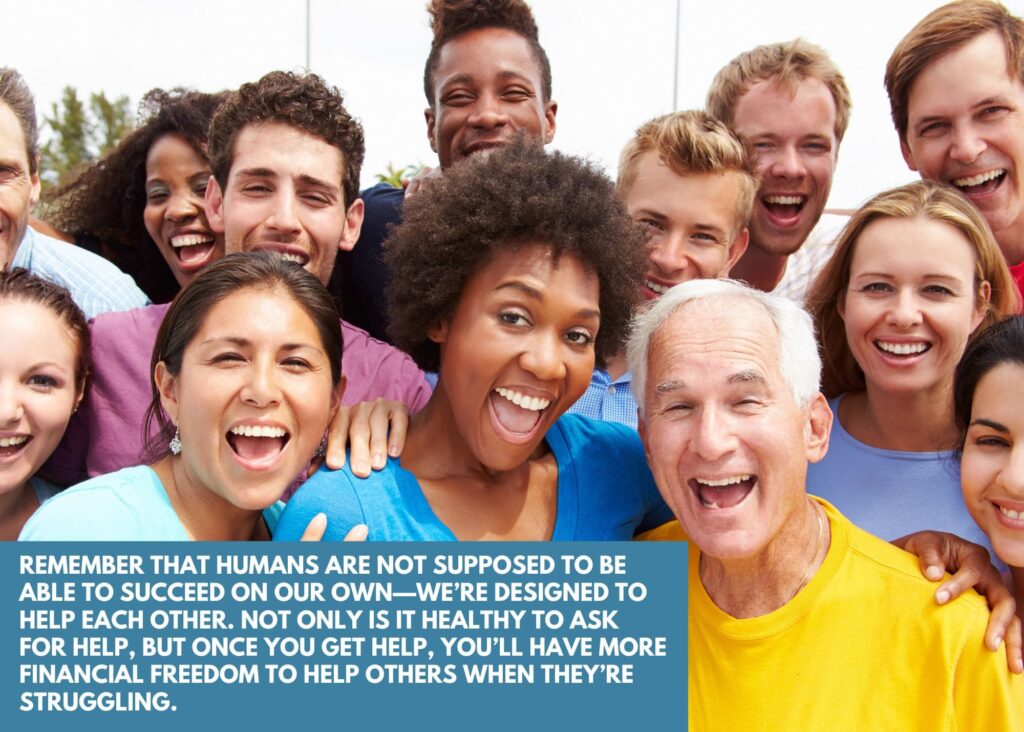

That’s when it’s time to remember that humans are not supposed to be able to succeed on our own. That’s right—we’re designed to help each other. Not only is it healthy to ask for help, but once you get help, you’ll have more financial freedom to help others when they’re struggling.

At RaiseUP Families, we’re passionate about helping families in the Houston area achieve financial independence so their children can have hope for a brighter future. If you need help with financial goal setting, here are the partners we recommend:

If you don’t live in Houston, you can find financial resources in your area by going to findhelp.org and entering your zip code. From the list of options that comes up, click on “money,” and then “financial education” to see a list of financial education resources in your area.

Remember, plenty of people have been in your exact situation and are happy to help you achieve a more financially stable future!

If you live in the Houston area and need help, feel free to contact RaiseUp Families! You may be a good fit for our HandUp program, and if not, we can connect you with the resources you need.