Do you have good credit?

That question might make you want to climb into bed and pull the covers over your head.

You’ve probably heard people say that you need good credit to get a loan, get good interest rates, or potentially even rent a home. But this may bring up questions you’re too scared or embarrassed to ask. Questions like, what even is credit? Or how do I improve my credit if I’ve made bad decisions in the past? Or how do I even start building credit?

Look, we get it. At RaiseUp Families, we know that getting finances in order can be frustrating and complicated.

That’s why we wrote this article, to break down the basics of credit so that you can feel confident as you work toward financial stability.

“Credit” is a term that refers to getting a loan or borrowing something. For example, it used to be common for businesses to let customers take goods “on credit” instead of paying immediately. Credit cards are the modern way to buy things with credit.

But credit is inherently risky for lenders.

Imagine a former classmate approaching you and asking for a $500 loan. Would you hand over the money or politely decline?

If your classmate was the type of person who always handed in assignments on time, paid their share of gas money when you drove to the beach together, and always returned books to the library before they were due, you’d lend the money in a heartbeat. But if they had a history of borrowing things and forgetting to return them, you’d think twice before handing them cash.

Now, imagine going into a bank and asking for a loan. Before the bank agrees, they want assurance that you’ll repay them. But they don’t know you and your character, so they rely on available information about other times you borrowed money.

This information is called your “credit history.”

If your credit history shows you reliably repay what you owe, you have “good credit.” And that’s important.

Why?

Let’s get into it!

In our modern financial system, it’s almost impossible to get ahead without some form of credit.

For example, let’s say you want to start a business. To pay for startup costs such as renting business space, purchasing inventory, and paying your employees before the profits start accumulating, you need a business loan.

Or, if you want to buy a house, you need a home mortgage loan.

If you play your cards right, these loans save you lots of money in the long run. A business loan helps your business become profitable much faster. Making mortgage payments might cost you about the same monthly amount as paying rent, but it’s all going toward a house you own and can re-sell. Whereas when you’re renting, that money is gone.

Having good credit gives you the following advantages:

If you’re freaking out because you know your credit history is terrible or because you’re not sure you have a credit history at all, don’t worry! We’ll help you out in a moment.

But first, let’s take a quick look at how “good credit” is calculated.

When you apply for a loan, credit card, or other form of credit, banks want to quickly and easily determine whether you have a history of timely payment.

That’s where your credit score comes in.

Your credit score is a number between 300 and 850. The higher the score, the better your credit is. Your score may differ slightly depending on which credit bureau is calculating it, but it’s based on the FICO credit score.

Your FICO credit score is calculated based on the following factors:

Now that we understand how your credit score is calculated, let’s discuss how that information can benefit you financially.

If you’ve never gotten a loan or credit card, you probably don’t have any credit history. But just to make sure, start by checking your credit score.

If you don’t have any credit history, it’s time to apply for a credit card.

The complicating factor here is that it’s sometimes hard to get approved for a credit card when you don’t have any credit history. If your credit card applications are rejected for this reason, you can get what’s called a “secured credit card.”

A secured credit card requires you to submit a refundable security deposit, proving you’re not a financial risk. Once you successfully build your credit by making timely payments on your secured credit card, you can move on to a regular, unsecured credit card.

As you can see in the breakdown of what impacts your credit score, the most important thing (35% of your score) is to make full, on-time payments. The second most important thing (30% of your score) is to keep the amount you owe low and spend less than your credit limit.

A “credit limit” on a credit card is the total amount the card lets you borrow without paying back. If you have a $1000 limit, you can spend up to $1000 before your card is declined. If you pay back $500, then you have $500 you can spend before your card is declined again.

For good credit, aim to use less than 30% of your credit limit.

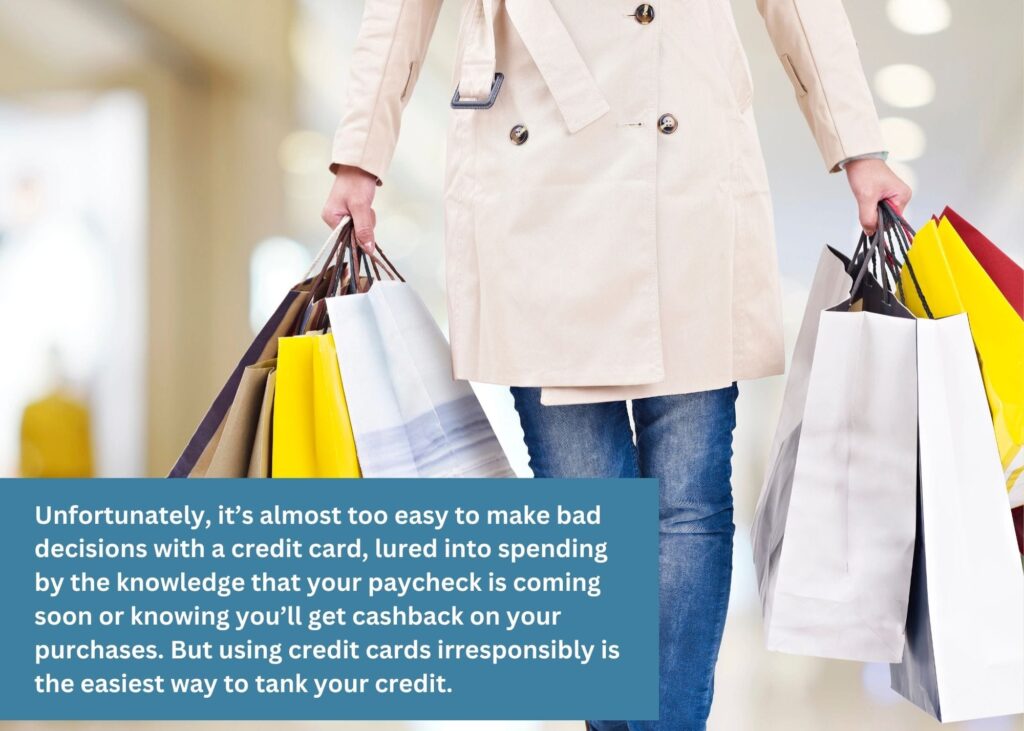

Unfortunately, it’s almost too easy to make bad decisions with a credit card, lured into spending by the knowledge that your paycheck is coming soon or knowing you’ll get cashback on your purchases. But using credit cards irresponsibly is the easiest way to tank your credit.

Instead, when you get a credit card, make a plan for using far less than your limit and paying in full every month. For example, if your card gives you good cashback at gas stations, use it to buy gas but nothing else.

Another good plan is to use your credit card to pay a subscription, such as Netflix or Spotify. Then, set up automatic payments to come directly out of your bank account and pay off your card each month. With barely any effort, you’ll use far less than your limit and pay in full every month, building great credit.

If you’ve tanked your credit by making bad financial decisions in the past, don’t worry; these are the steps you can take to improve your credit!

Step 1: Check your credit report for errors

Three main credit bureaus collect and compile your credit information: Experian, Equifax, and TransUnion. You can get a free copy of your credit report from each of these agencies each year.

Unfortunately, sometimes there are errors on your report. An easy first step to improving your credit score is to look at your credit report and dispute any errors you see.

Step 2: Get help

If you want to improve your credit, you need to start making better financial decisions. Unfortunately, that’s difficult to do! But the good news is, there are plenty of people and agencies out there willing to help. We’ll go into more detail later, but for now, remember that you’ll do much better improving your credit if you have support than if you try to go at it alone.

Step 3: Pay your bills on time

Remember, the main chunk of your credit score is based on your payment history, so start making timely, full payments, and your credit score will start improving.

Step 4: Pay down debt

Once you’re paying your bills on time, the next step is to pay off your debt. This journey takes time and commitment, but remember, there are agencies in your area waiting to help you build good financial habits and make debt repayment a reality!

Bonus: Remember how earlier, we talked about getting a secured credit card as a way to build credit when you have none? Well, you can also use a secured credit card to rebuild good credit after you’ve tanked your credit store.

This blog gave a general overview of understanding credit, but when it comes to building and maintaining good credit, the best thing you can do is find local resources that will help you learn to manage your finances well.

Here at RaiseUp Families, we help parents in the Houston, TX area who are experiencing financial hardship to provide a stable home for their children. We know that one key to stability is to learn to manage your finances and improve your credit score!

Here are some organizations we partner with and recommend:

If you’ve enjoyed this article and are interested in reading more about financial stability, you may be interested in our other blog posts, including:

And remember, if you’re struggling to keep your family’s head above water financially, feel free to reach out to RaiseUp and get help!